Private investment in the space sector declined by 58 percent in the year 2022, according to a new Space Investment Quarterly report from the firm Space Capital.

The $20.1 billion in private market equity investment last year is the lowest annual total since 2015, said Chad Anderson, the founder and managing partner of Space Capital. While early stage investments were largely unchanged, the large decline came in late- and growth-stage companies.

The report cites several factors for the pullback, including the fastest interest rate hike cycle since 1988, a challenging investment environment, and a continued economic recovery from the COVID-19 pandemic.

However, Anderson told Ars that another factor was the relatively poor returns of space-based companies that have gone public via the Special Purpose Acquisition Company, or SPAC, process, dating to 2019 when Virgin Galactic did so. According to an analysis by SpaceWorks, $100 invested in a “new space” index of stocks in January 2021 would be worth about $15 today, compared to $127 for a traditional space stock index.

SPACs whacked

“The poor performance of SPAC companies has certainly influenced investor attitudes,” Anderson said. “This is just one of several factors influencing investor sentiment, but it definitely is significant. Amid the general pullback in technology investing, space companies are often viewed as a higher risk category, and SPAC underperformers like Virgin Galactic are clearly driving those perceptions.”

Anderson said it typically takes about six to eight years for a company to progress from its initial round of seed funding to an initial public offering of stock. By this yardstick, many of the space companies that have gone public via the SPAC process did so prematurely—not just pre-revenue, but in some cases pre-product.

Some of these companies, such as Virgin Galactic, Virgin Orbit, and Momentus, still lack a viable commercial product years after going public. While these companies may have needed public funding to survive their early development years, this additional scrutiny has made innovating much more challenging.

“It is difficult to build a core product, fail, pivot, and innovate as a public company,” Anderson said. “The public markets prefer operational stability and predictable revenue. It’s no wonder that many of these companies have disappointed.”

Focus on fundamentals

With that said, Anderson believes that some SPAC companies are beginning to demonstrate their viability. Moreover, he said, there are some “incredible” space companies that have been working in the background for several years. These companies will be ready to go public, via a traditional initial public offering, within a few years.

As for other notable tidbits in the report, Anderson called attention to SpaceX’s capital raise of $2 billion in 2022, the company’s second-largest annual raise. SpaceX has sought this additional funding as it has worked to bring two large development projects—the Starlink Internet constellation and the Starship launch system—online.

Space Investment Quarterly

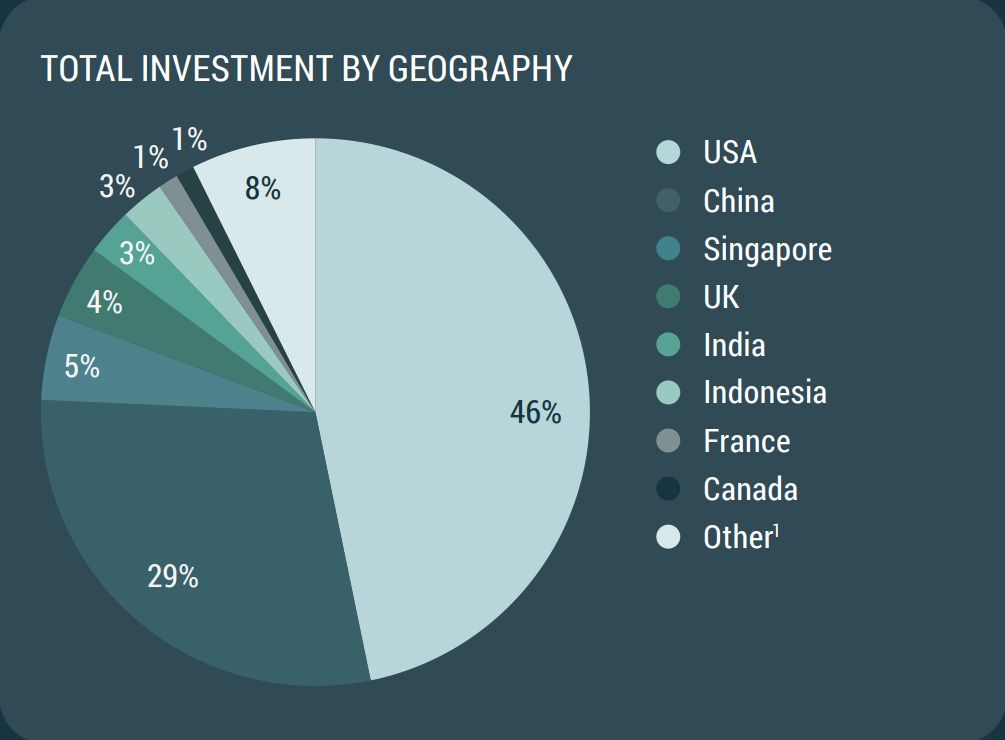

China also appears to be closing the gap to the United States in private investing in the space economy, Anderson said. Chinese companies have attracted 35 percent of all Space Applications investments, for example, compared with 41 percent for US companies. This is being driven by China’s e-commerce and location-based services boom.

Looking ahead to 2023, Anderson sees another difficult year for space startups due to the lack of investment capital available for small companies to draw upon. However, he views a shift from “momentum investing” to a greater focus on fundamentals as a positive trend, which will benefit quality space companies in the long run.

{kind=link}